To the average consumer, few things seem more simple than a cup of coffee—just add water (and/or milk and sugar). For those of us on the other side of the equation, however, the feeling tends to be the exact opposite: there are few things that seem less simple than coffee. This is especially true once you’ve plunged down any one of coffee’s many deep and cavernous rabbit holes. From growing to roasting to brewing and beyond, each aspect of the industry can contain a seemingly endless combination of factors and variables to consider.

But while it’s safe to say that most people generally understand the “macro” steps of coffee (that a farmer grows coffee which must then be roasted before being brewed by your method of choice) minus the technical details (e.g., processing methods, roast curves and extraction yields), when it comes to the role of the C Market and how green coffee is purchased, it’s not as straightforward as, say, going to the supermarket and picking up a bag of tomatoes. Unless you’re a seasoned coffee trader, understanding the C Market can be an entirely different ballgame.

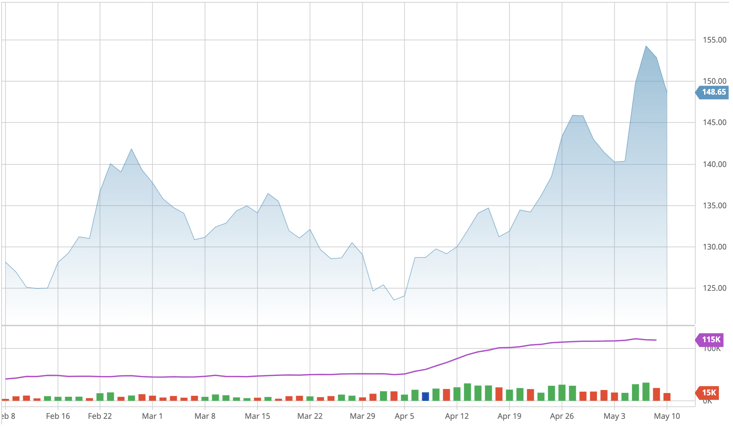

Given the recent rise in coffee prices—which we break down in this recent webinar—we thought we’d take a moment to go back to basics. In this post and a few more to come, we’ll be going over exactly what the C Market is, how it works, what determines the price of coffee and the price that farmers actually receive.

________________________________________________

What is the C Market?

The C Market is the global exchange in which the world’s Arabica coffee is bought and sold—i.e traded—every day. If you’re thinking that sounds like a financial market or stock exchange—you’re absolutely correct! Like sugar, wheat, cotton, oil, or gold, coffee is considered a commodity, and the back and forth flow of selling and buying is what informs the ever fluctuating price of coffee, or “C” price.

Fun fact: the “C” in C Market actually stands for “centrals” and not “coffee” or “commodity” as some think. The modern C Market that we know today was established in 1968-1969 by producers in Central America who were looking to differentiate their prices, mostly from Brazilian beans. Before the C Market, Arabica coffee was traded under the Universal or “U” contract. Today, coffee producing countries around the world trade their Arabica beans on the C Market, not just those from Central America.

.png?width=1040&name=C%20Market%20101%20(1).png)

Coffee is a commodity—but what does that mean exactly? In global commerce, a commodity is considered to be a raw material or input that is generally used in the manufacture of other products. Commodities are also interchangeable with other goods of the same type, e.g., a barrel of crude oil produced in Texas has the same application as a barrel of oil extracted in Saudi Arabia. Quality is essentially considered uniform across commodities of the same type (we in specialty coffee know that this is definitely not the case, but more on that later).

In the case of coffee, coffees that are allowed to trade on the C Market must meet certain quality standards: coffee must be Arabica, unroasted, produced in one of twenty predetermined countries, exchanged in one of eight warehouses around the world, and traded in quantities of about 37,500lbs (or about the size of one shipping container). For Robusta, a separate market exists.

This is important to note: one of the primary functions of the C Market (or any commodity market) is to standardize the trade of coffee and set the rules for trading.

Why Does the C Market Exist?

So why the need for a complex financial market for something like buying and selling coffee (or sugar or wheat or any commodity) in the first place? Why (and how) are commodities traded like stocks and bonds?

Commodity markets actually predate the advent of the stock market by hundreds, if not thousands, of years, and are intimately connected to the rise and fall of entire civilizations who depended upon the efficient trading of goods. While we’re not diving into that long history, the commodity markets we know today arose from two key developments in commodities trading: the spot market and the futures market.

The spot market is where the actual physical sale of a good happens, and it’s called the spot market because transactions are settled “on the spot.” This is what comes to mind when we think of a traditional marketplace with vendors hawking their wares and buyers paying in cash.

There are two inherent problems with the spot market, however: liquidity and price discovery. In the spot market, the flow of goods can often be inefficient and unstable—a seller doesn't always have a guaranteed buyer and the market conditions can be uncertain. Furthermore, until the seller actually brings their goods to market, they have no idea what the going price is for the goods they are selling, and are only able to assign a price based on what everyone else is selling for.

On top of this, it takes several months for a farmer to farm her crop before she brings it to market. In that time, a number of events can happen that could drastically affect the price: a snapchill might reduce harvests and increase prices, or an unexpected bumper crop could significantly increase supply and drive prices down. Of course, this uncertainty also affects buyers.

To solve this problem, producers and buyers began entering into “futures contracts.” Both parties would agree to exchange commodities at a later date—in the future—but the terms of the exchange would be settled first, on that day. This practice eliminated uncertainty, and over time, futures contracts became the main way that buyers and sellers would deal.

There was, however, a new problem: accounting for instances when one party would back out of the deal, usually due to going bankrupt. A buyer no longer able to purchase goods from a producer would be leaving that producer high and dry and at the mercy of the spot market.

The C Market of Today

Enter: the futures exchange. In coffee, this is what we now know as the C Market, currently operated by the Intercontinental Exchange (ICE) where coffee futures are traded.

The exchange acts as a centralized, third “counterparty” to the buying and selling parties, with the main advantage being that the exchange can’t go out of business (under normal circumstances). Rather than buying and selling directly, a seller sells to the exchange, and a buyer buys from the exchange.

The exchange also addresses the problem of liquidity. By working through the exchange, sellers are essentially guaranteed a buyer for their product and vice versa. In a liquid market, a high volume of transactions are able to occur quickly and easily, and participants are able to efficiently open or close their positions.

-1.png?width=734&name=DSC00893%20(1)-1.png)

Trading futures contracts on the exchange also allows both parties to exit contracts if and when they need to. For example, take a buyer who has contracted a container of wheat from a farmer. If, at some point, the buyer wants to exit the contract, they can simply sell it to the exchange where it will be bought by another person. They just have to make sure that they sell the contract before it expires because whoever holds the contract at the time of expiry will be receiving the physical delivery of the goods contracted.

This means that in every commodity market, there are a large number of participants—otherwise known as investors or “speculators”—who never actually deal with the physical trade of the goods themselves, but buy and sell contracts just like one would buy and sell stocks. The activity of these non-industry market participants can have a huge influence on the price of coffee, but their activity is crucial to maintaining market liquidity. Learning to navigate this is, in fact, a key part of farmer risk management and hedging contracts.

One last but very important thing to note about the C Market and the C price: when it comes to specialty coffee, the C price is not the final price that a farmer is paid for their coffee, but merely makes up a portion of that price. The reality is that because all coffee is considered a commodity, the C price applies to all Arabica coffee, regardless of quality or cup-score.

However, what's crucial to understand is that the C price simply acts as a reference, "benchmark" price for coffee and that, for specialty coffee, differentials based on country, quality and certifications build upon that price and play a huge role in making up the final amount that farmers are paid. Understanding how these differentials factor in to pricing will be the topic of a later post!

________________________________________________

In case some of this was a little hard to grasp, here are the main takeaways when it comes to understanding the “what” and “why” of the C Market:

- The C Market is a global commodity exchange—similar to a stock exchange—where both the physical trade of green Arabica coffee and the trade of coffee futures contracts occurs.

- Not all coffees are traded on the C Market. To be traded, coffee must meet certain standards.

- Like a stock exchange, the C Market standardizes exchanges and sets rules for who can trade and how trades occur. In addition to those involved in the actual manufacture of products from green coffee, there are market participants who exclusively deal in buying and selling contracts.

- The C Market provides a global benchmark price for coffee. While other factors also influence the final price that buyers pay for coffee, the fact there is a price reference is essential. Without the C price as a benchmark, determining the price of coffee on a global scale would be very difficult.

- The C Market acts as a centralized counterparty; buying and selling contracts through the market helps to ensure market liquidity and the flow of coffee.

This is, of course, a very barebones breakdown of a wildly complex topic (there are people who go to school for years to learn how to effectively trade in commodities!), but it should hopefully provide a frame of reference for our later posts in this series where we’ll be taking a look at a number of topics including: causes of market volatility and factors that influence the C price; how we help farmers manage their risk in the market; the impact of local market prices, differentials, and certifications; how exchange rates affect producers; farmgate pricing and what prices producers actually receive.

Be sure to subscribe below to be updated for the next posts in this series!

.png "SH Logo")